The Oil Problem

The Great Recession has depressed the price of oil as fewer people commuting and less goods being shipped around has meant less demand at the gas pump. This has been a blessing to the economy, which is already reeling from high unemployment and excessive debt loads. But what happens when the economy starts to pick up again? Or worse yet, what happens if the rest of the world starts to churn ahead while we continue a long, slow decline?

Oil is a commodity traded in dollars in a global market. The supply/demand curve applies so when the economy is slow, there is less demand for oil. This is particularly true when the slowdown is in the country that has the highest oil consumption rate in the world. As National Public Radio noted last week:

Crude prices have retreated nearly 8 percent in the past two weeks as the U.S. economic newsflow has generally underperformed. At one point on Thursday, oil prices fell to a six-week low below $74 a barrel after figures showed an unexpected rise in weekly U.S. jobless claims to half a million, and a big drop in manufacturing activity in the Philadelphia region.

Lower U.S. economic growth means that unemployment will remain higher and factories will need less energy than many traders had been predicting as oil prices recovered from the depths of recession.

Fewer jobs also mean fewer people filling their tanks to drive to work and fewer holidaymakers.

So the recession has meant lower oil prices. This does not automatically mean that an end to recession will mean higher oil prices, but there is reason for concern. As stated by Steven Kopits, a managing director for an energy consulting and research firm, the oil/recession feedback loop can set the conditions for a "continuous recession".

If Kopits is correct, so much for "green shoots." They will be trampled under foot over and over again unless there is a sudden spike upwards in GDP growth disproportionally more so than oil price increases.Here is the roller-coaster cycle he points out: Higher oil prices mean recessions, recessions mean less consumption then lower oil prices, which leads to less exploration and supply which leads to higher oil prices and recession again.

Kopits is an icon of sorts in the Peak Oil debate, which we are not going to get delve deeply into here. Regardless of what you believe in the peak oil discussion, Kopits' analysis is something worth pondering. If the economy picked up and, for whatever reason, we saw gasoline at the pump shoot up over $4 per gallon again, it is hard to see the recovery lasting. Without sustained high oil prices, there is little incentive for companies to spend capital on research, exploration and new drilling systems.

In other words, in our current oil-dependent configuration, it is difficult to see how a recovery gets any long-term traction. Recession depresses oil prices. Low oil prices depress exploration and development. Lack of exploration and development means that, when a recovery happens, we'll be faced with shortage of supply relative to demand. The resulting higher prices will create another round of recession.

That analysis assumes an American-centric world. Let's ponder for a minute the impact of a place like China on this analysis.

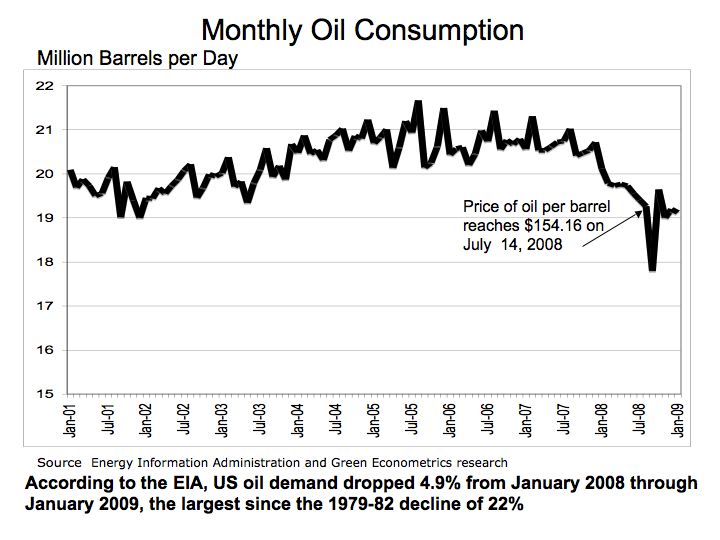

The U.S. rate of oil consumption has fallen from peaks seen pre-recession.

This trend is not happening in China, which is in the process of transforming its economy from third world to first. Imagine 300 million Americans driving cars. Now imagine 300 million Chinese driving cars and understand: that is just one of four of them. Here's a chart of their consumption:

And China is just one of a number of developing countries. India and Brazil along a with a huge consortium of emerging markets are also increasing their energy consumption as their standard of living rises. Will these economies drive demand - and the higher prices - that justify the capital expenditures to bring more oil to market? Or, more ominously, what if these places drive up the price independent of the American economy, forcing higher energy prices upon us while our economy is still faltering?

There is one other interesting wrinkle here, and it ties back to the original NPR article we quoted at the beginning of this piece. As reported by NPR:

Oil industry analysts Cameron Hanover have even warned that crude prices should be substantially lower — below $35 and potentially as low as $10 a barrel based on the weak state of demand.

"Prices are near $75 instead because investors — gargantuan investors — are pricing oil more in terms of gold than in terms of the market's history, the euro, the dollar, or supply and demand," it said.

"It is good to see oil prices sell off on Thursday but it is a deck-chair off a cruise ship. Prices should be substantially lower, based on record supplies during a recession with no timetable for recovery," it added.

Let me state that in a different way. Our economic situation is so tenuous that "gargantuan" investors are buying oil because it will hold its value (like gold) when other things (like the dollar) do not. Gulp. That does not exactly inspire confidence.

What does this all mean for towns and neighborhoods? At the very least, the more oil-dependent the local economy is the less resiliency that town has. Local initiatives for economic growth can be overwhelmed by energy volatility that the community has no ability to control. And energy volatility looks likely. Places wanting to be Strong Towns need to be reconfiguring themselves to reduce their exposure to this obvious source of volatility.

Unfortunately, at the state and federal level we've used this recession to spend trillions on the current development pattern, doing little to address our oil dependency. From a land use perspective, the emphasis on "shovel ready" projects has meant that we've simply taken the existing auto-centric development pattern and given it an injection of steroids. This is a recipe for long-term disaster.

A final word on Peak Oil. I think there is little question that the theory behind Peak Oil is sound; all oil deposits peak in their rate of return as oil is removed and the deposit becomes diluted. This lowers the rate of return over time once the "peak" rate is reached. That part is simple physics and we've seen it demonstrated ever since we started extracting oil from the ground. The real debate is over whether we have reached global peak already, will reach it in a decade, in a century or longer. Depending on your belief in the timetable, you may or may not think we can drill/explore out way out of any oil shortage.

While important to policy makers looking at the economy over the next few years, resolving the Peak Oil debate is not critical to a Strong Towns approach. Our towns and neighborhoods in their current configuration are dependent on cheap fuel. No town can do anything to control the price of gasoline. Given these facts, a Strong Towns approach would have the community build resiliency against the inevitable volatility.

How? Grow the local economy through import-replacement (reduce import-dependency). Adopt living patterns that do not require automobile travel for everyone for nearly every trip. Develop alternative energy sources locally.

Our current homogeneous development pattern has made us all susceptible to the same shocks. Become a Strong Town and break the cycle.

The Strong Towns Blog; It's like reading Jim Kunstler, except you can share it with your mom. Sign up for a Curbside Chat, our project to bring the Strong Towns message to towns and neighborhoods across America. You can also join us on Facebook and Twitter.