Dumb Money, Day 4

The inspiration for this entire series was a set of people who, independently, expressed to me that there were thinking about either (a) investing in the stock market or (b) buying a home. All cited recent reports of upward trends in the price of stocks and houses as justification for their moves.

I've also experienced a lot of enthusiasm for municipal investments to induce growth, borrow more money to get things going and essentially get back to the economy of 2005, which is going to happen really soon for those that get in the game. I also wanted to shatter this delusion.

And finally, I'm just so frustrated with the narrative from the Krugman Keynesians. As they hold out the king-sized candy bar and tell everyone that, if we just ate another, the sugar rush would get us up off the floor and we'd then have the strength in our economy to prosper. It's true, we can get up off the floor with another candy bar, but a lot of good, prudent and innocent people are going to get slammed hard when the sugar rush goes away. Statements to the contrary are comforting and convenient, but ultimately are reckless and harmful.

Neil21 is a long time reader and someone I've become a friend with here. I'm looking forward to heading out to BC later this year and meeting him in person. We do, disagree, however, on this topic. Here's a statement he made yesterday to summarize his contention:

Abundant capital is a great thing.

On it's face, that is clearly true. For an economy, abundant capital will provide for investment and growth. Continuing with the human body analogy (another complex system), it is a little like saying "energy" is a great thing. When we have a lot of energy, we can accomplish a lot of things.

(I'll also note here that too much capital causes inflation while too much energy causes hyperactivity and insomnia -- abundant capital/energy has limits, for certain, but what we're talking about here is a lack of sluggishness.)

We all understand that a body can get energy in productive ways and unproductive ways. Good sleep habits, a healthy diet and plenty of exercise is the healthy way for a body to have energy. This requires discipline and balance and, even when it is not pleasant, it requires one to listen to their body. That sore muscle is telling you something; maybe you need to stretch it more, or make sure it isn't neglected in your routine. That headache is a good thing if it is warning you that you are dehydrated.

So the human body, a complex machine, experiences volatility and gives off warning signs when things are not optimal. Sometimes we can respond to those signs in a way that is clearly productive -- we can drink more water or alter our exercise to be more balanced -- but sometimes we have to resort to other means. We can't solve a torn ACL with diet and exercise; for that we need some surgery followed by some antibiotics and pain killers.

He's the fine line; we all understand that we ultimately need to shed the pain killers. Even Ben Bernanke and Paul Krugman will say, we ultimately need to shed the pain killers -- the low interest rates and quantitative easing -- and let this patient (a sick economy) learn to walk again. The trillion dollar question is: when?

This gets me back to the statement I made on Tuesday.

So, in normal times, we must save to invest.

Savings is the diet and exercise of a healthy economy. We save money -- delay the immediate reward of consumption -- for the promise of a greater future reward. These savings, in turn, can be productively invested by others today, resulting in growth. The natural regulator between savings and investment is the interest rate.

What economic stimulus does -- whether it is manipulation of the interest rate, printing of money or deficit spending -- is to give us investment without the need for savings. So we get energy without the need for a healthy diet and exercise.

We can see how, in an emergency situation or on a really bad day, it might be convenient to drink a Red Bull or eat a candy bar to give ourselves an energy boost. A steady diet of Red Bull and candy bars, however, can only lead to disaster.

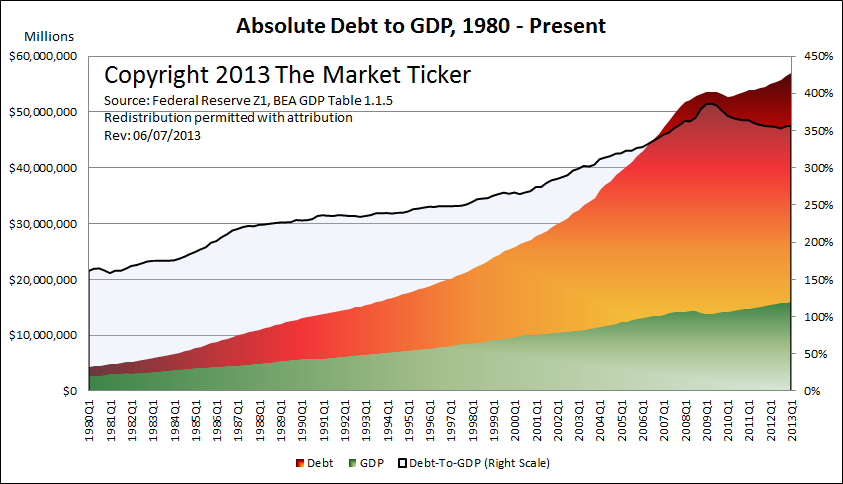

I'm going to finish Day 4 with three graphs that show how the steady, sixty year diet of Red Bull and candy bars every time our economy has felt a little sluggish has deformed our economy. I particularly want to give some context to the recent stock market highs and housing data.

Here's our overall economic growth as compared to debt. As we proceeded through the second life cycle of the Suburban Experiment, the lack of real productivity in the economy was replaced with Red Bull (debt). This kept the economy going, allowed us to continue to grow our GDP, but allowed us to also become increasingly unproductive. By 2005, the height of the housing boom, our ability to sustain growth was almost entirely based on Red Bull (debt) and even then, we needed to grow debt at a faster rate than the economy just to manage meager growth.

The gains we are seeing now in the stock market -- paper gains -- are not based on real productive growth. They are largely the result of cheap credit, something only sustainable so long as the Red Bull continues to flow at accelerating amounts. The crowding out of real savings by the Federal Reserve also means that people are being enticed into stock markets as a way to have any earnings at all. Although people have been shown to be unwilling to gamble where they can lose, when the momentum shifts and perceptions change, people are more than willing to gamble when they believe they will win.

The gains we are seeing now in the stock market -- paper gains -- are not based on real productive growth. They are largely the result of cheap credit, something only sustainable so long as the Red Bull continues to flow at accelerating amounts. The crowding out of real savings by the Federal Reserve also means that people are being enticed into stock markets as a way to have any earnings at all. Although people have been shown to be unwilling to gamble where they can lose, when the momentum shifts and perceptions change, people are more than willing to gamble when they believe they will win.

In terms of housing, this was the chart that brought together everything that I'm seeing. We've been treated to the media reports that median homes prices are rising. This graph shows how this relates to median incomes.

In short, home prices might be rising, but it is not a product of us having an economy where people are making more, earning more and having more money to invest in housing. It is an artificial creation of cheap credit. If we were transitioning to a real economy -- something stable -- that graph should be trending down, not up.

And finally, we must save to invest. As we got into the second life cycle of the Suburban Experiment and the growth from horizontal expansion slowed, we replaced savings with Red Bull, putting off a difficult conversation about the wisdom of our approach and, in the process, creating an even larger deformation that we will ultimately have to deal with.

This is an incredibly fragile economy. That fragility is not the construct of recent bailouts, natural economic cycles, greedy politicians, a prolific consumer, lazy freeloaders, the 99%, the 1% or any of the other groups we like to pin the blame on. It is the result of sixty years of deformation, of responding to the aches and pains with Red Bull and pain killers.

Yes, that approach - what has evolved into a supply side, Keynesian amalgamation -- allowed us to grow faster, much faster, than we otherwise would have. It allowed us to live large, have an enormous standard of living, and accomplish many, many things that we would not have been able to do were we not taking economic steroids.

Smoothing of the business cycle and decades of this faux-prosperity has all come at a price, however. That price is a great unwinding. On Day 5, I'm going to provide an optimistic roadmap for how a great unwind could happen. On Day 6, I'll give a less generous version.

(Note: I'm taking next week off to work on a private writing project, attend some girls softball games with a 8 year old and a 6 year old and get caught up. We'll have content here on the blog, but continuation of this series might be on hold until I get back.)