Albuquerque's Hidden Deficit

This piece was originally published, in slightly different form, on Downtown ABQ Lab. It is shared here with permission.

[[divider]]

Albuquerque is heading into budget season. If you’ve followed these before, you know what to expect.

High emotions, tense exchanges, and often tears as councilors grapple with painful decisions: what to cut, which promises to not deliver on, and which of their constituent’s needs to leave unmet. The yearly ritual of proposing cuts to our library’s budget, only to restore it after public outcry. Insults and accusations at perceived injustices over a project being funded in one district but not another. Emotions run high because everything feels—and is—essential. Nothing feels optional. And yet decisions need to be made. Needs go unmet. Life-and-death services and infrastructure go unfunded. The reality of a city barely keeping up is hard to miss.

And yet, open Albuquerque’s official financial report and you’ll see a completely different picture. One of a city worth nearly $4 billion. A wealthy city. A city that feels almost surreal as you sit through budget deliberations. So what gives?

An honest look at the numbers, especially how roads and infrastructure are counted, reveals a very different story. A bleaker view of our city’s financial standing. One that actually matches what we see and feel during budget season. A city over $1 billion in the hole, barely able to tread water.

Net Position: $3.7 billion

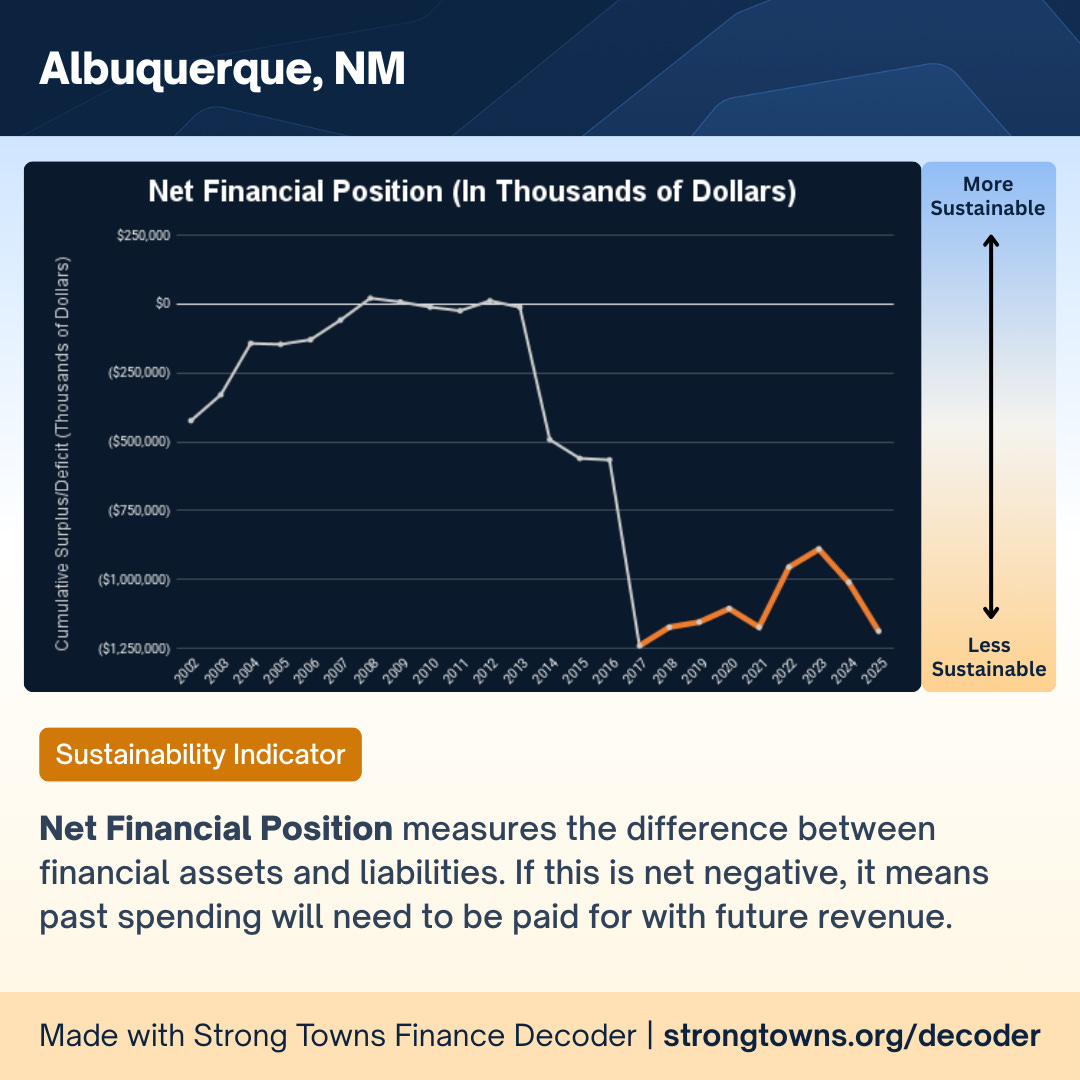

Net Financial Position -$1.2 billion

Yes, this is a post about municipal finance. Not exactly thrilling stuff. But stick with us.

1. A Wealthy City

The $3.7 billion figure comes from the City’s official Net Position.

net position = assets — liabilities

This is the municipal equivalent of net worth in personal finances: what you own minus what you owe.

- Assets: house, savings, investments, retirement account, car

- Liabilities: mortgage, student loans, auto loan, credit card

Simple.

Things get trickier when we apply this idea to a city. What counts as an asset? What counts as a liability? In the United States, those rules are set by the Governmental Accounting Standards Board (GASB), which standardizes how governments report their finances.

Sounds legit, why shouldn’t we take this at face value?

Turns out accounting rules matter more than one would think.

When GASB updated its standards in the 2010s to require pension and retiree benefit obligations to be fully counted as liabilities—as they should be—cities across the country suddenly appeared more indebted overnight. Albuquerque’s reported liabilities jumped by more than $1 billion. The city hadn’t actually taken on new debt. The reporting rules changed.

Financial statements don’t just reflect reality. They reflect the framework used to measure it. We already had those obligations, they just weren’t being fully counted before.

And even today, GASB’s Net Position still obscures some very real liabilities.

2. Roads: Assets or Liabilities?

The biggest issue with GASB’s accounting framework is that it treats roads and other municipal infrastructure as assets. That’s problematic for two reasons.

First, a road is not an asset in any practical financial sense. An asset is typically something that can be sold or leveraged to pay off debt1. You can sell a house. You can liquidate investments. But you can’t dig up a road and sell it to the next town over if you run into financial trouble. When cities default, creditors don’t seize streets or water pipes and auction them off.

Second, roads don’t just fail to function as assets, they function more like liabilities. Liabilities beyond the initial debt to build them. Every mile of pavement represents an implicit long-term obligation to maintain, repair, and eventually replace it. In perpetuity.

If we were accounting for municipal infrastructure properly this would amount to a double whammy, removing an asset from the positive side of the ledger and adding a liability to the negative side.

The real asset behind infrastructure isn’t the road itself, it’s the tax base the road supports, which already shows up in the city’s finances as revenue.

3. A Broke City

In 2009, the Canadian Public Sector Accounting Board (PSAB), the counterpart to GASB, issued Statement of Recommended Practice 4: Indicators of Financial Condition. It recommended evaluating governments using additional metrics grouped into three categories: sustainability, flexibility, and vulnerability. Together, these provide a more holistic view of financial health than a single balance-sheet number.

One of those metrics, the Net Financial Assets (if positive) or Net Financial Debt (if negative) provides an alternative to GASB’s Net Position. One that circumvents the “road problem.”

Rather than attempting to reclassify infrastructure (i.e. accounting for it “correctly” as Strong Towns advocates for), this metric simply excludes capital assets altogether.

Cities already classify their assets as either financial assets or capital assets2.

- Financial assets: cash, investments, receivables

- Capital assets: roads, buildings, equipment

assets = financial assets + capital assets

The Net Financial Position focuses only on the resources that can actually be used to pay obligations:

net financial position = financial assets — liabilities

This reflects a basic reality: cities pay their debts from revenues and liquid resources, not by selling roads or city hall.

And here’s where the picture changes dramatically. Albuquerque’s Net Financial Position is −$1.2 billion (debt).

That means our financial obligations exceed our financial assets by more than a billion dollars. And this isn’t even the most unsettling part.

4. The Hidden Debt

The Net Financial Position tells us whether we can pay our bondholders. It tells us whether we have more financial assets or financial debt. It removes roads and buildings from the asset column, which makes sense. We can’t sell them to pay debt.

But infrastructure creates another kind of obligation. Not to investors. To residents. Every mile of road is a promise to maintain, repair, and eventually replace it. That obligation doesn’t show up as a formal liability on the balance sheet. But it’s real.

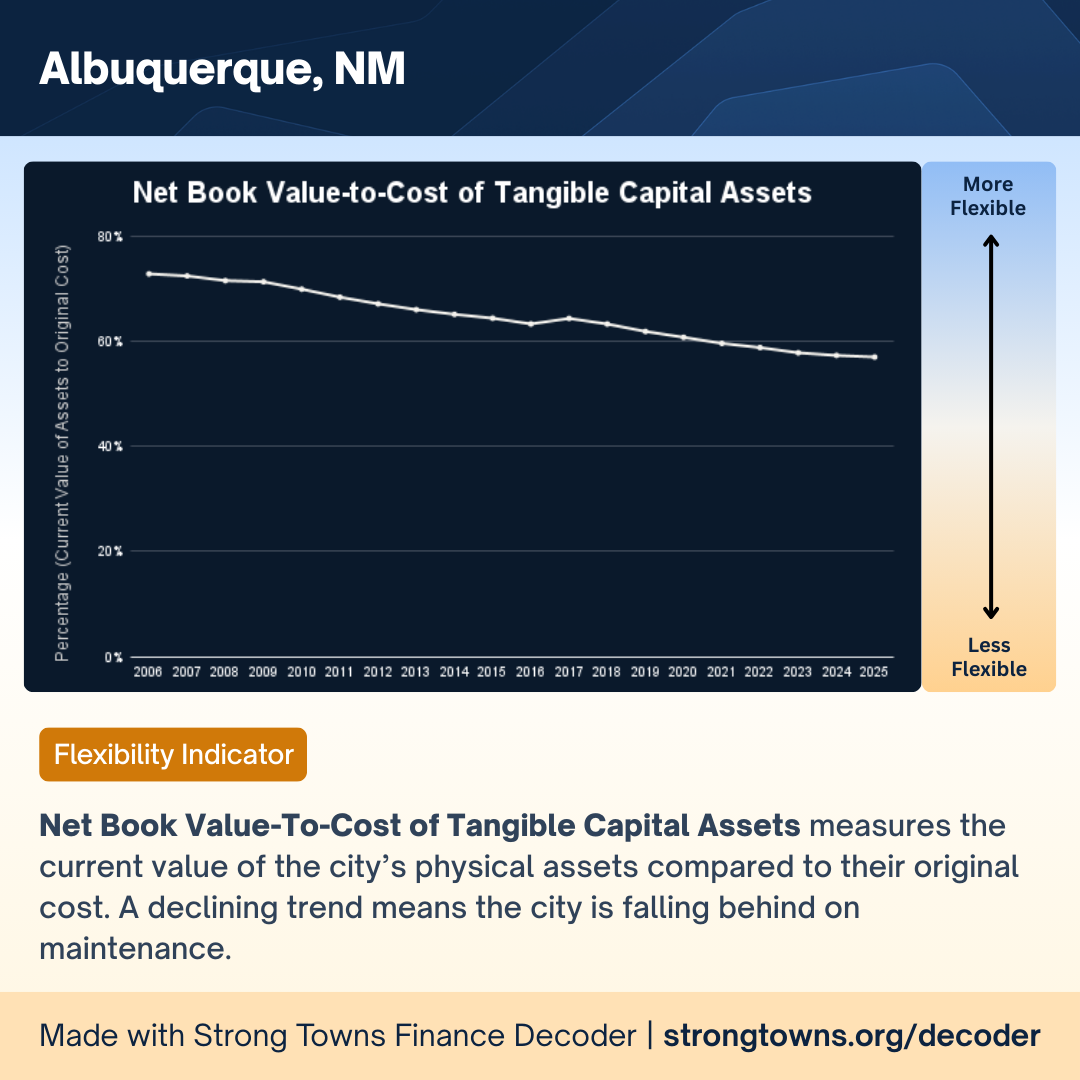

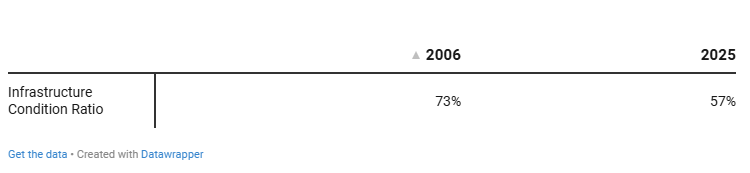

The Strong Towns Finance Decoder captures this with a simple metric with a not-so-simple name: Net Book Value-to-Cost of Tangible Capital Assets, which we will just call the Infrastructure Condition Ratio. It is how much our infrastructure is currently worth in its current condition compared to how much its full value is.

infrastructure condition ratio = current value / full value

Cities already track both numbers. They record the original full value of infrastructure. They also depreciate roads and buildings as they age and restore their value as they are repaired.

If infrastructure were maintained evenly over time, this ratio would stay roughly flat. Instead, Albuquerque’s infrastructure condition ratio has steadily declined. In 2006, our infrastructure was valued at about 73% of full condition. Today, it’s 57%. Deterioration is outpacing maintenance. The city is not keeping up.

That 43% gap represents deferred maintenance: infrastructure that exists but has not been fully maintained. In dollar terms? That’s roughly $3.5 billion in maintenance backlog. This isn’t a formal debt owed to bondholders. But it is a real obligation. And it exists on top of our $1.2 billion net financial debt.

5. Who Are the Real Stakeholders?

Albuquerque is a municipal corporation. Like any corporation, it has stakeholders. Turns out the answer to who those stakeholders are sits at the heart of the discrepancy we’ve highlighted.

The mission of any city is to provide its residents a safe, prosperous, functioning place to live, and to do so sustainably, in perpetuity. You’d be forgiven for thinking, like us, that residents are therefore the principal stakeholders. And in some ways we are. We elect leaders and hold them accountable at the ballot box. But when it comes to how we measure, track, and report our finances, the city’s ability to deliver for residents is not part of the equation.

Who is the financial report for then?

Bondholders.

These are investors, mutual funds, endowments. The Annual Comprehensive Financial Report (ACFR) answers one question: Will the city repay its debt? And the city answers clearly: Yes.

Debt is always paid first. Before roads are repaired. Before services are expanded. If the budget is tight, services are cut, infrastructure goes unfixed, debt is repaid.

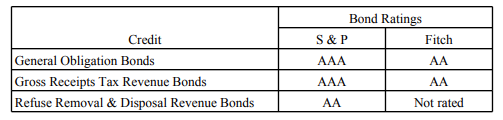

From that perspective, the financial report makes perfect sense. The glossy cover pages, reporting awards, and AAA bond ratings from Standard & Poor’s signal to investors that Albuquerque is a safe bet.

Clear reporting and transparency matter. Bonds are an important tool. But they are just that, a tool to fulfill the city’s true mission—serving its residents. Somewhere along the way, that priority blurred. When we only measure what matters to investors, it becomes the only thing that matters.

Perhaps we should measure financial health in a way that reflects our obligations to residents, not just lenders. What is our ability to deliver on those debts? And they are debts. A metric like the Infrastructure Condition Ratio makes this visible. The numbers are already there, buried in hundreds of pages of financial statements, these metrics simply surface them.

If we don’t track them, we get what we have now: a rosy financial picture while infrastructure deteriorates and services are cut. We are in a state of slowly worsening soft default and we don’t even see it coming because we are not measuring the right things.

Many cities, including Las Cruces (though notably not Albuquerque) publish a Popular Annual Financial Report (PAFR) with residents as the intended audience. These reports make city finances more accessible, summarizing them in clear tables, graphs, and plain-language explanations. That’s a meaningful step toward transparency. But the core metric remains Net Position under the GASB framework, which does not reflect the city’s ability to deliver to residents.

Albuquerque should publish an annual popular report.

More importantly, Albuquerque should adopt and track a set of metrics that offer a more holistic picture of how the city is serving its residents, and its ability to continue doing so into the future.

Because the real bottom line isn’t our bond ratings.

It’s whether our city works for the people who live here.

[[divider]]

1. Strictly speaking, assets do not need to be sellable. In accounting, assets are resources expected to provide economic benefit and can include intangible items such as software, easements, or permits. In practice, however, non-sellable assets are usually a small share of the balance sheet. Municipal infrastructure is different. Roads and similar assets make up the vast majority of many cities’ reported assets, even though they cannot realistically be liquidated to meet financial obligations.

2. There’s a third Other Assets category that includes things like intangible assets. This is usually negligible compared to capital and financial assets. For the Net Position metric Other Assets are lumped in with Financial Assets so that only Capital Assets are excluded. In the Albuquerque ACFR the combined non-capital assets are called “current and other assets”.

Carlos Michelen is a research engineer working on marine renewable energy at a U.S. Department of Energy national laboratory. He helps lead Strong Towns ABQ, serves on Albuquerque’s Transit Advisory Board, and sits on the board of his neighborhood association. Carlos lives in Albuquerque’s Huning Highlands neighborhood and is passionate about building financially resilient cities and walkable neighborhoods.

Benjamin Bean is a computer vision researcher by day, dad by night and on the weekends, and is a Strong Towns advocate whenever he can be. He sits on the board of his local Neighborhood Association and is a frequent sight at city council meetings. Ben can frequently be found at one of the many amazing coffee shops in downtown Albuquerque.

%20(1).avif)

%20(1).avif)

%20(2).avif)

%20(1).avif)