A Fiscal Cliff?

%20(1).avif)

%20(1).avif)

.avif)

%20(1).avif)

%20(1).avif)

Recently, The Observer ran a headline: “Commissioner calls Manatee County ‘poor’ during workshop sessions.”

I said it on purpose because I want people to understand what we’re actually dealing with in Manatee County, Florida, not the press-release version of our finances, but the real version. When you look at what we’re obligated to pay, what we’re continuing to build, and what we’re failing to set aside for the future, “poor” is not a dramatic exaggeration. It’s an honest description of our current, and more importantly future, trajectory.

Let me explain how I got there.

The Strong Towns Finance Decoder Summit

I was invited to participate in a two-day work session with Strong Towns, an organization I’ve followed closely for years and genuinely believe in. In fact, when I became Chair in 2025, I handed all our commissioners the first Strong Towns book to help start better conversations about how cities and counties grow, spend, and plan. This work session was conveniently right after our first round of budget meetings (June 8–10).

Strong Towns pulled together a small group of 15 people. Charles Marohn (who runs the organization) was there with some of their staff. The rest of the room was a mix of people who live in this world every day: real estate tech industry, a professor, community activists running local Strong Towns conversations in places like Chicago and Albuquerque, and three elected officials (a councilwoman from Colorado, a mayor from Minnesota, and me).

The focus of the session was their “Financial Decoder”; a tool built to help municipalities and counties understand their real financial position. Not the political version. The real one: what we owe, what we’re taking on, what’s sustainable, and what isn’t. For two full days, we did intense presentations, discussions, and problem-solving to sharpen the tool so communities can better see shortfalls coming before it’s too late.

The timing felt almost ironic. Everything we were discussing in that room maps perfectly to what Manatee County (and honestly most counties) are dealing with right now. After COVID, federal and state dollars flowed in fast. Departments expanded. Projects moved. Assets got built. Then the extra money dried up. Now we’re left with bigger systems to run and maintain but fewer outside dollars to help carry the load. Sound familiar?

To contribute to the work session, I ran Manatee County through the Financial Decoder myself. That meant pulling every single Comprehensive Annual Financial Report (CAFR) going back to 2009 and entering the data so we could see the long-term trend lines clearly. The output is a set of charts that make it hard to hide from reality.

What the Charts Actually Show

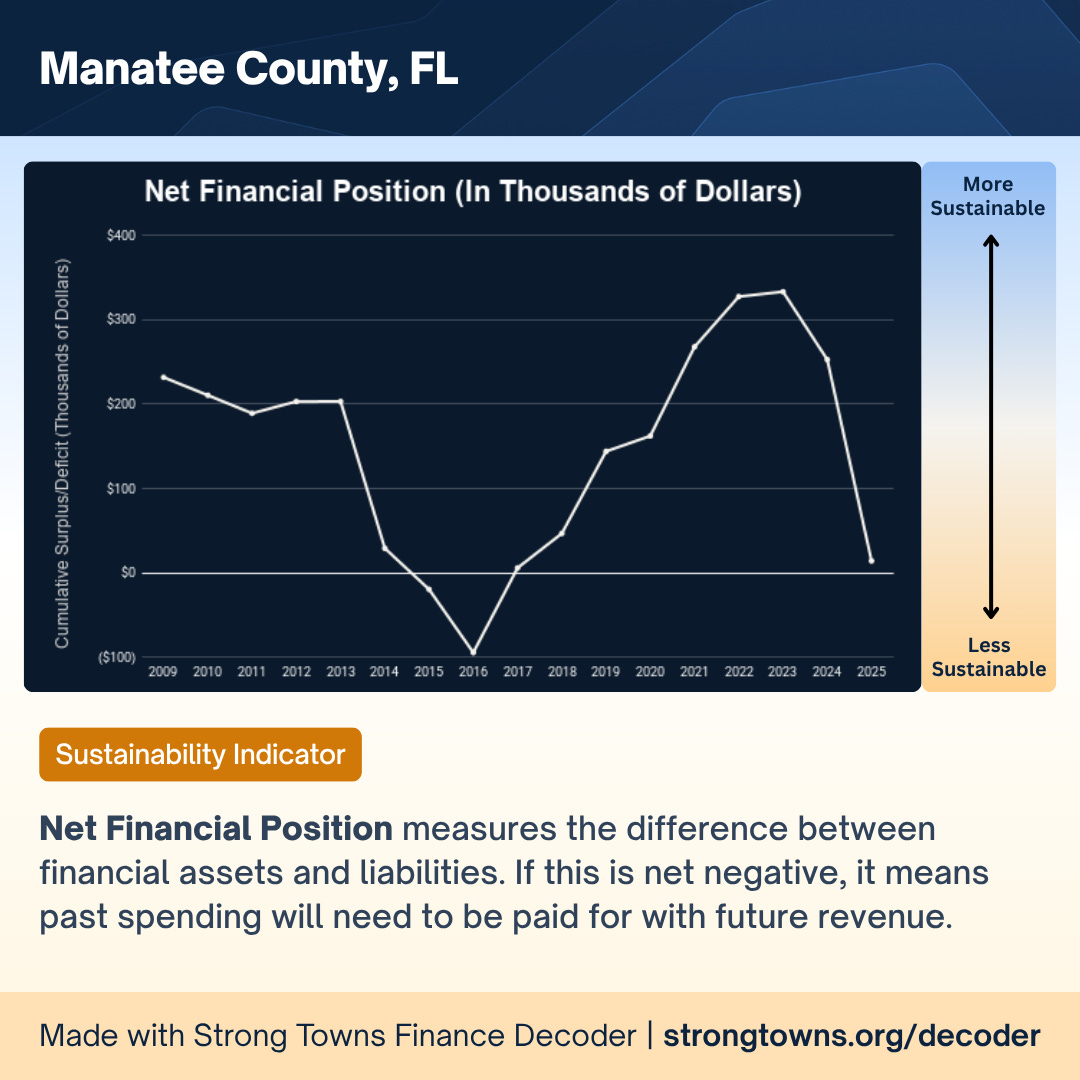

Let’s start with our net financial position.

Net financial position is the difference between our financial assets and our liabilities. When it goes negative, past spending has to be paid for with future revenue. You can see that after a COVID-era spike, driven by stimulus and federal dollars flowing in, the line has dropped hard and is approaching zero. That is not a good direction.

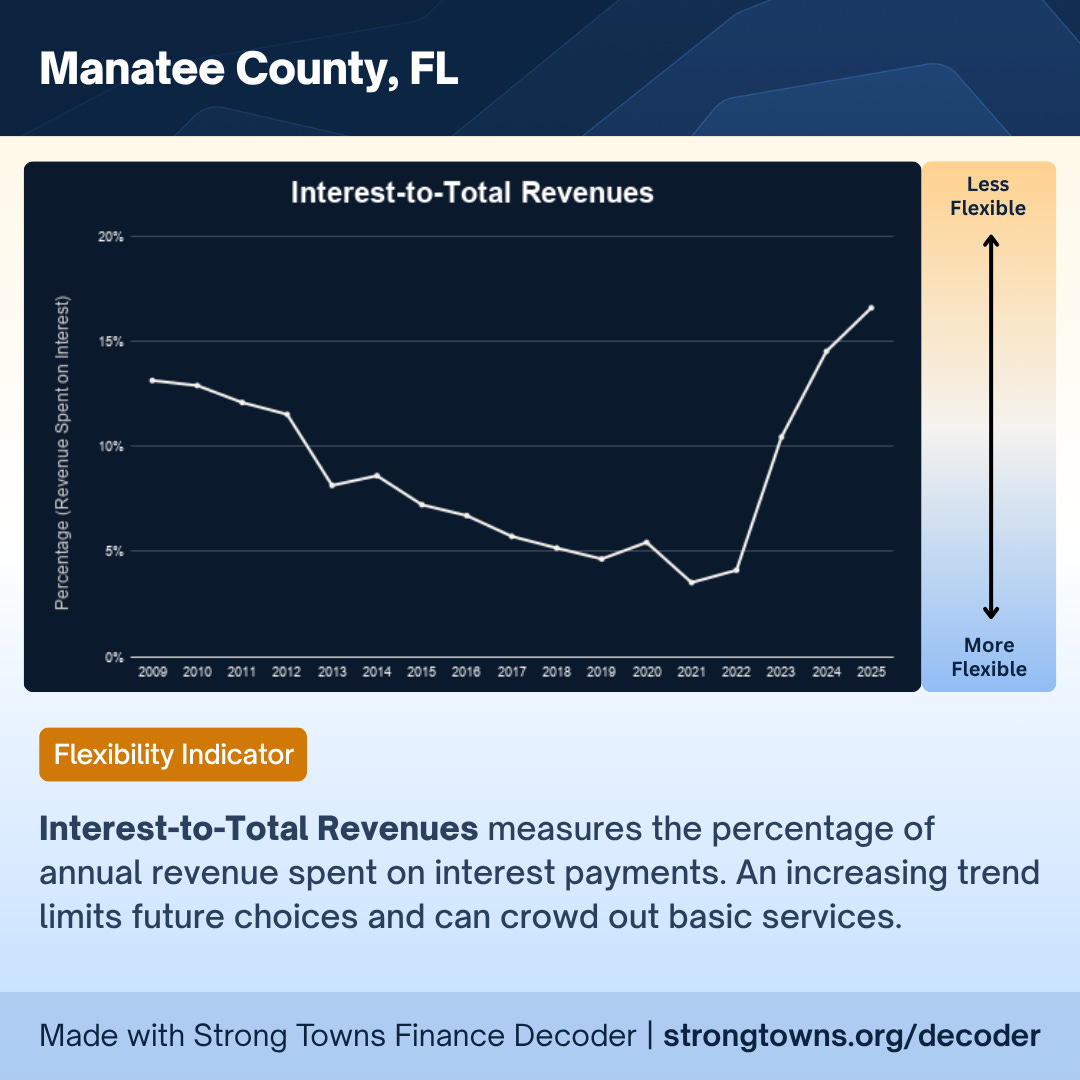

The second chart shows interest-to-total revenues, which measures how much of our annual revenue goes toward interest payments on debt. When this rises, it limits future choices and begins crowding out basic services.

After years of improvement, the line turned sharply upward starting in 2021 as we bonded more for infrastructure to catch up with the inflow of population. Debt service is now our second-largest budget line item. Second only to the sheriff.

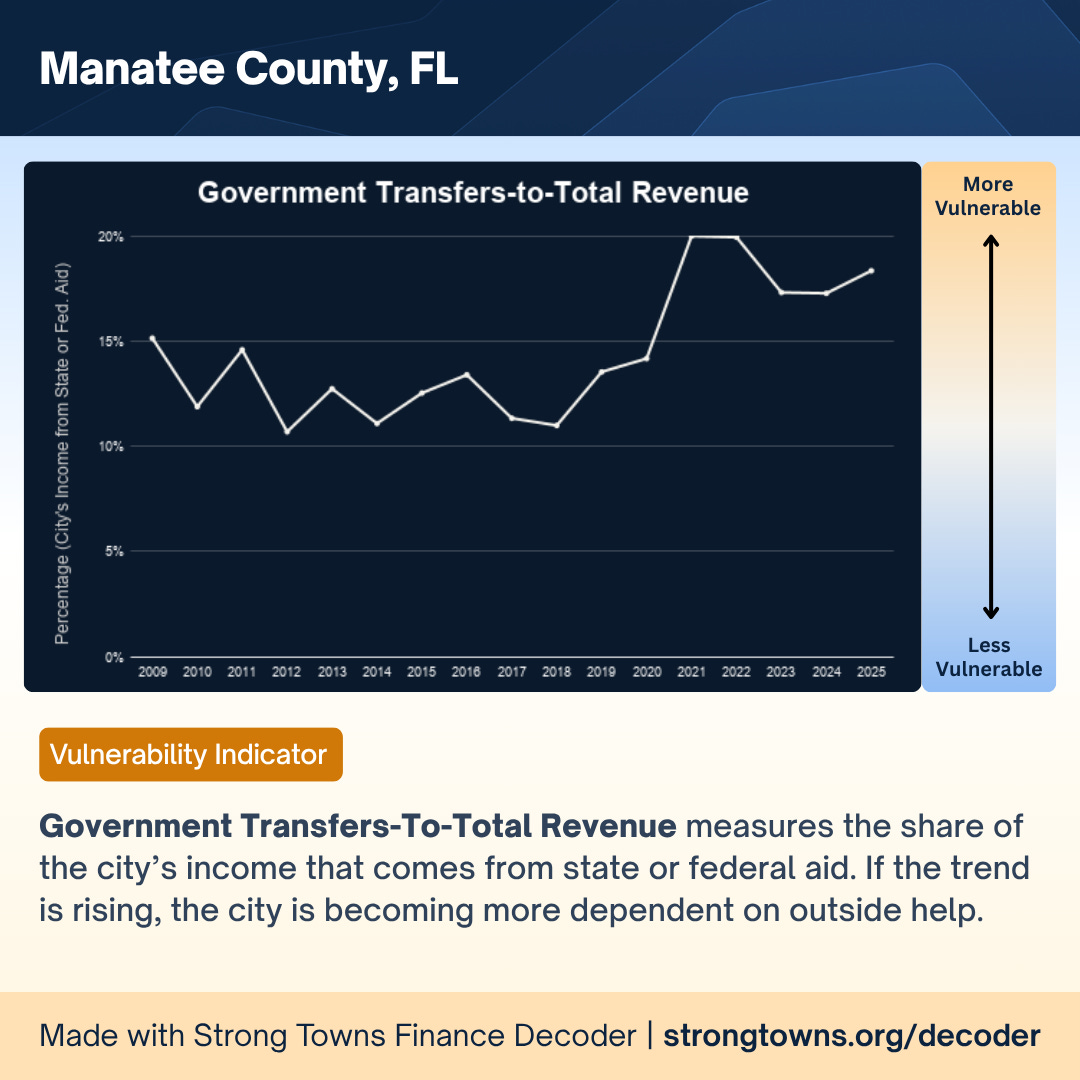

The third chart shows government transfers as a share of total revenue. Basically, how reliant we’ve become on outside funding from the state and federal government.

You can see the reliance climbing, particularly post-COVID. The problem: once those appropriations slow down or stop it will create holes in projects that assumed the money would always be there. And Tallahassee is already signaling tighter budgets and projected shortfalls at the state level in the coming years. This isn’t hypothetical.

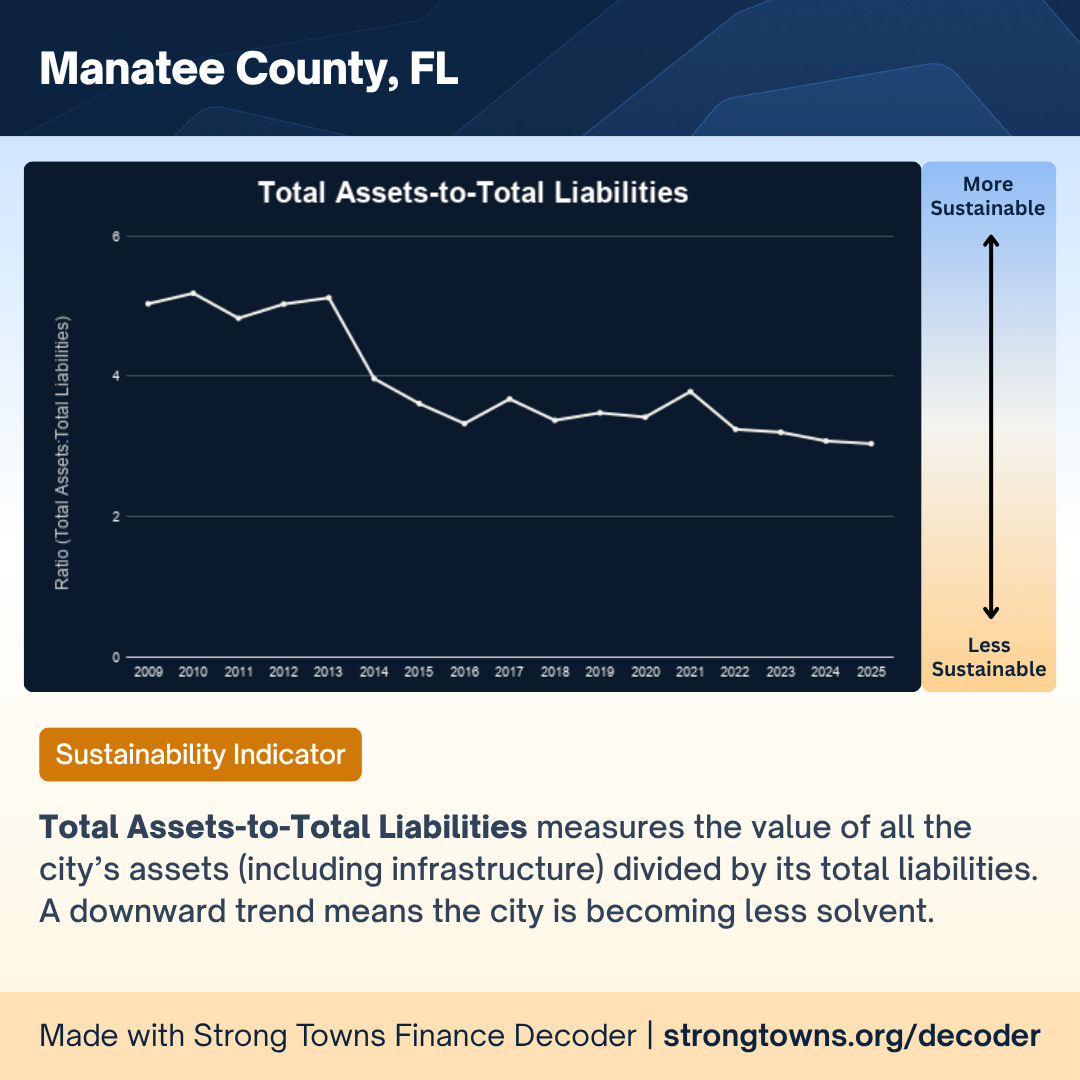

The final chart brings it all together: total assets-to-total liabilities.

A downward trend here means the county is becoming less solvent over time. Our ratio has been in near-continuous decline since 2013. It has not reversed. The chart continuously goes the wrong way and the trend looks to continue.

The Reserve Cliff

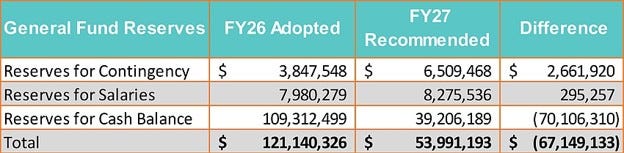

Now let’s get specific to the Manatee County budget sessions for fiscal year 2027, because this is where the word “poor” becomes clearer.

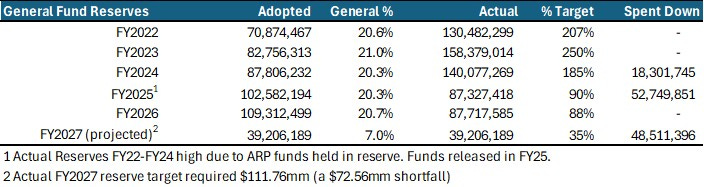

The most immediate red flag is our reserves. Our county’s reserve policy recommends we maintain 20% of the general fund balance in reserves. Last year (FY26), the reserve was adopted at $109.3 million. This year (FY27), we’re being told our available reserve for cash balance is only $39.2 million, a drop of more than $70 million.

Based on the policy target, our reserves should be $111.7 million this year. We’re sitting at roughly $39.2 million. That means we are approximately $72.5 million short of our own policy requirement. Sitting at about 7% when the policy says 20%.

That is not a small miss. Those reserves are the cushion that keeps services running when the economy turns. And Manatee County is cyclical. We’re heavily reliant on construction, tourism, and service industries. When the economy slows, those slow and revenue can drop fast. Reserves are what keeps the lights on (sometimes literally) when the bottom falls out.

Reserves also aren’t just a nice-to-have. They’re not meant to be treated like a spare checking account. Once reserve dollars are gone, they’re gone. And if you spend reserves on recurring services, those dollars don’t create an asset you can point to later. You just have fewer reserves and the same ongoing service expectations.

What’s especially frustrating is that holding reserves is one of the few things that’s actually easy to maintain once you do it. It’s not like a new program that requires fresh annual funding forever. If you keep reserves at the proper level and avoid tapping them for day-to-day spending, you’re not constantly scrambling to “find” reserve money each year. But we haven’t done that, and now we’re in a deep hole.

If we stay on the current path, we’re heading toward a situation where reserves go $0 in another year. But “a sustained decline in general funds reserves” is a key factor in our credit rating (presently Moody’s: Aaa; Fitch: AAA) and a drop in these ratings will negatively affect our ability to, and our cost of, borrowing in emergencies. That’s why I’m sounding the alarm now, not later.

The reality is that we’ve simply been spending down reserves to cover non-emergency obligations. This is partly a result of recent millage cuts. Since 2021 we’ve lowered the millage rate by 0.70, a reduction of more than 10% across five tax cycles. The cumulative impact of those cuts is roughly $116 million less in property tax collections. That number is larger than the reserve shortfall we’re staring at.

We made up for reduced taxes by supplementing operating costs with our rainy day fund. And now the rainy day fund is nearly empty right as it’s getting cloudy.

In spite of what the State CFO may say on his campaign roadshow, Manatee County has not overspent $112 million in tax dollars. In fact, we’ve done what they want and went to the rollback over time to the detriment of our budget. The county portion of my tax bill has only increased $114 total over five years, or 0.016% of the appraiser’s market value of my home.

Through this analysis, however, I do agree that we’ve overspent since COVID. But that has come from excess spending of our healthy reserves and shortsighted capital project investments with non-recurring appropriations leaving us with increased future liabilities.

The Maintenance Cliff

Then we get to the conversation nobody wants to have in a county that keeps building new roads: can we actually afford to build more if we cannot maintain what we already have?

Manatee County has about 3,600 lane miles (roughly 1,538 center lane miles — the length of roads regardless of number of lanes). A straight-line estimate puts road maintenance at roughly $17,500 per center lane mile per year, or about $26.9 million annually just to maintain existing roads. The ones we already have. Not anything new.

In theory, gas taxes should cover most of that. We collect approximately $25 million in gas tax revenue. But last year we only spent about $19 million on maintenance. That means we underfunded road maintenance by roughly $8 million (about 30% of the maintenance that “should” have happened did not happen). And with roads, deferred maintenance doesn’t stay flat. It gets worse. It compounds. It gets more expensive.

And that’s before we add a single new lane mile.

We currently have over 35 miles of new roads under construction. When those come online, they will add roughly $600,000 per year in new maintenance obligations on top of the $8 million per year gap we’re already carrying.

People want those roads (our total transportation projects in the capital improvement plan are about $1.6 billion in future assets-turn-liabilities). I get it. But the question isn’t whether they want them or need them. The real question is where will the long-term maintenance money come from before we obligate future residents to additional unfunded burdens?

So Where Will We Make This Up?

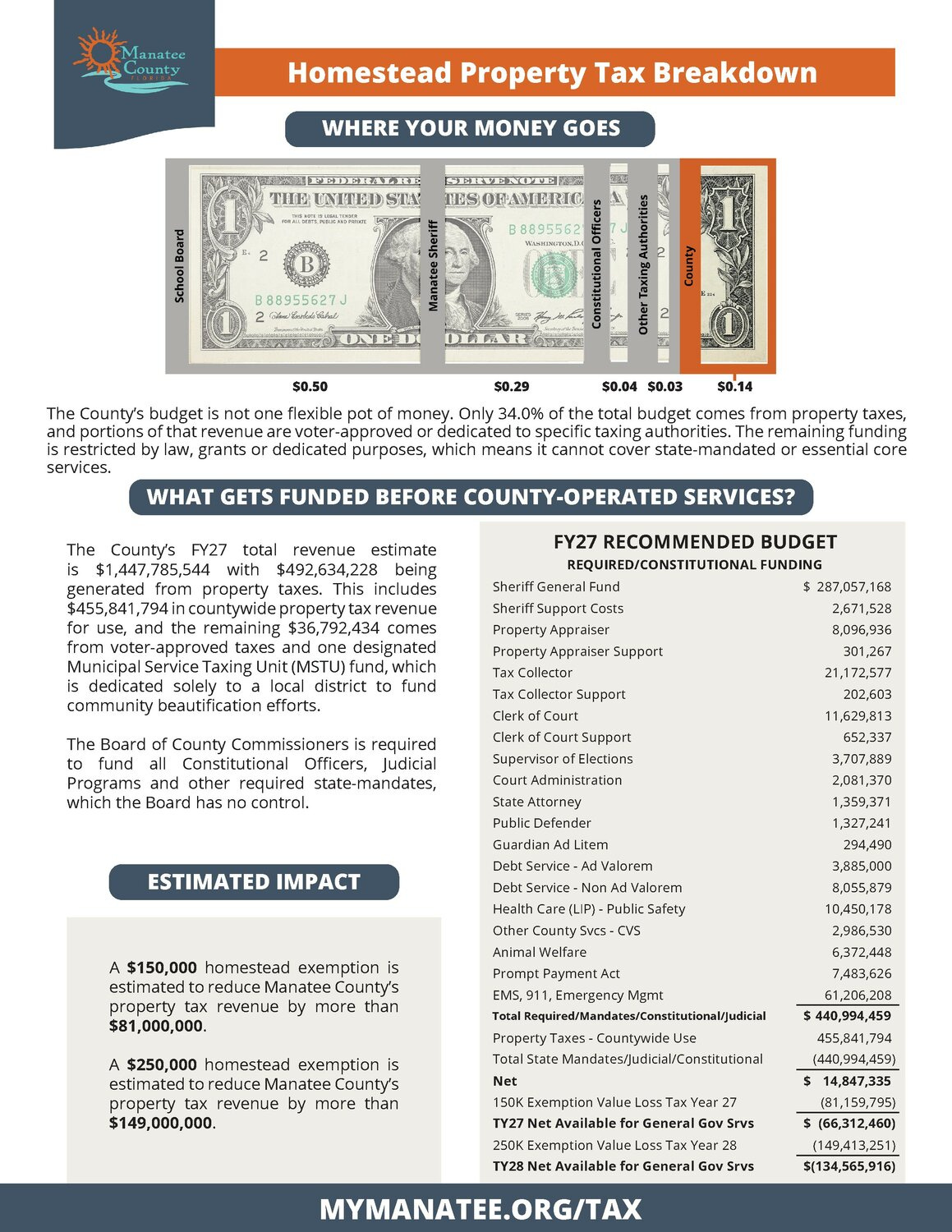

The county’s gross budget this year is about $2.67 billion. That sounds enormous. But gross budget is deceptive as it includes internal transfers between departments, multiple reserve categories (impact fees, landfill, and more), state and federal appropriations, gas taxes, tourist development taxes, capital projects, and over a billion dollars tied to utilities (an enterprise fund that is almost entirely outside the property tax conversation people are actually having).

When you strip it down to what most people mean when they say “the county budget,” the operating budget is closer to about $500 million. And within that, the constraints are tighter than most residents realize.

During budget week, we went through, in detail, exactly how much of our general operating fund is essentially required or state-mandated spending. That includes the sheriff (by far the largest share at over $287 million), the other constitutional officers, court-related obligations, contractual debt service, mandatory EMS and 911 emergency management, and healthcare-related costs. We don’t get to wave a wand and make those go away. But we can nominally lower the amount we allocate to them.

The total required/mandated spending comes to roughly $441 million. Our total property tax revenue countywide, net of referendum millages for children services and environmental lands, is approximately $456 million. Once those mandatory obligations are paid, according to our CFO, we have roughly $15 million left for everything else — parks, libraries, veteran services, transit, boat ramps, road maintenance, and every department residents interact with on a daily basis.

To really put the financial problem into focus: if we cut every single non-mandated service (all of them), without adjusting funding for mandated services, we’d free up that $15 million. Even if we put all $15 million into reserves, we’d still only get to around $55 million in reserves, roughly half of what our policy recommends.

That’s why I said the situation is serious. The math simply doesn’t work without hard decisions.

The Math That Defines the Problem

If you combine the reserve shortfall and the maintenance reality, you start to see the size of the challenge.

Even if we agreed to gamble on accepting a reserve shortfall for the next half decade, to rebuild reserves over five years, we’d need to find roughly $15 million per year for five straight years to fully-replenish the account. Add the $8–10 million per year we’re short on road maintenance and we’re looking at roughly $25 million per year that needs to be found just to stabilize the fundamentals. This is before we expand a single service. Before we commit to a single new project, road, or initiative.

But remember, we only have about $15 million of flexible, “discretionary” funding after mandatory spending. Even eliminating every single non-mandated service gets us nowhere near the $25 million we need just to stop the bleeding.

This is the textbook definition of a structural financial problem.

This is the full context behind my “poor” comment. It doesn’t mean Manatee County is broke today. It means we’ve been spending like the good times would never end - using one-time money, building new assets, expanding services, and lowering millage — without fully accounting for the long-term costs of what we’re creating.

It also means we are more exposed than most people realize if the economy turns. And we are well past the point in the cycle where a downturn is unthinkable. If property values drop, construction slows, tourism dips, or the state tightens appropriations, our budget pressure becomes immediate. Without reserves, the options get painful fast.

We Are Not Alone in This

The Strong Towns work session made one thing clear above everything else — we’re not unique. Many communities are in the exact same spot. They used the COVID-era funding surge to build, expand, and just say yes to many niceties, all while many cut taxes to help their residents in an inflationary economy. Now they’re back to regular, normalized revenue with bigger obligations and smaller cushions.

This is not unexpected nor is it historically unique. Every community, every economy goes through cycles. Some cycles are strong and allow for growth and expansion. Some cycles are negative and require us to make the decisions necessary to weather them. Some are caused by external factors. Some are caused by internal decisions. But, just like with 2009, we will get through it, right the ship, and move forward.

The question now is whether we deal with this cycle proactively, clearly, honestly, and in a structured way, or we kick the can a few more fiscal cycles and leave it for a future board to confront in a even worse situation.

One path is uncomfortable but manageable. The other is far worse.

In the weeks ahead, this conversation needs to get real. If we want to keep our AAA credit rating, maintain safe roads, protect quality-of-life services, and restore our reserves to where our own policy says they should be, we have to face the math.

That likely means some combination of adjusting spending, slowing down new commitments, rethinking how we build, and having an honest conversation about revenue.

The numbers won’t fix themselves. And waiting only narrows our options as we attempt to avoid the cliff.

Next Steps

- Diligently look at reducing operating expenses, mandated and non-mandated, to free up limited discretionary funds.

- Create a plan to replenish reserves, immediately or over a fixed timeline.

- Take inventory of current assets and create a sustainable plan to ensure sufficient funding for maintenance.

- Reassess how we budget for future capital assets to ensure long-term funding for maintenance prior to committing ANY current capital on new CIP projects.

- Watch the November ballot initiative and prepare to make even tougher decisions for FY2027 and beyond if passed (just imagine this discussion with $81 million in lower revenue in 2027 and $149 million less in 2028).

If you want to explore the Strong Towns Financial Decoder for Manatee County or your own community, the tool is free and publicly available at strongtowns.org/decoder.

[[divider]]

This article was originally published, in slightly different form, on Strong Towns member George Kruse's Substack, Policy 68. It is shared here with permission.

George Kruse is a second-term county commissioner in Manatee County, Florida, with a focus on growth management, affordable housing and multimodal transportation. He sits on numerous advisory boards, including the Florida Association of Counties, the Affordable Housing Committee, the local MPO, the Chamber board and many others. In his spare time, he advises on origination for short-term bridge financing nationwide for a NYC-based hedge fund. He started in commercial real estate with a LIHTC syndicator and went on to CRE finance on Wall Street before moving back to Florida. He graduated with a BS in Finance from the University of Florida and with an MBA from Columbia Business School. He's active with ULI Tampa Bay as well as housing policy work at both the state and federal level.